The Annual Sticker Shock vs. The Monthly Drip: Making Sense of California Insurance Payments

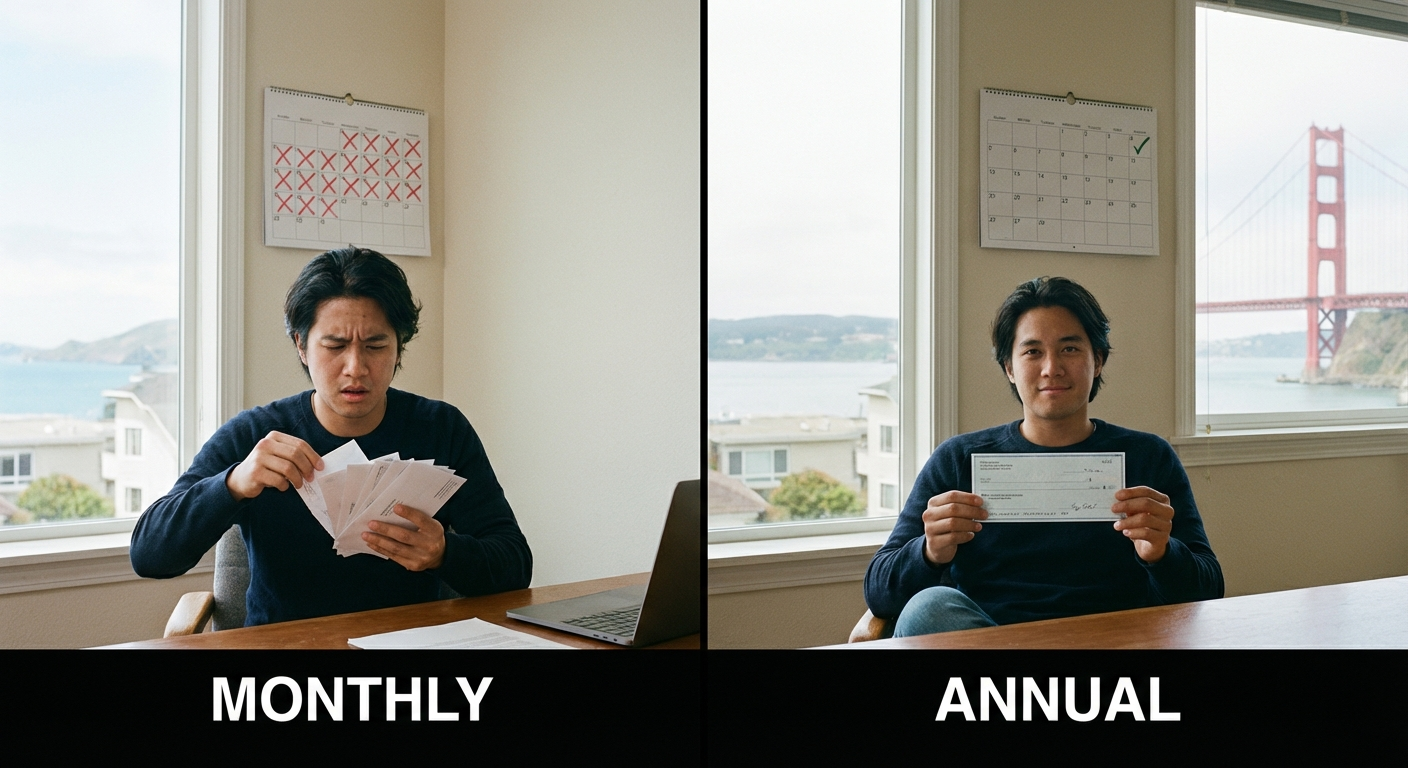

The Chengs, like so many families across California, felt it every year. Their home insurance renewal notice would land in their mailbox, a thick envelope from State Farm, usually around the same time the Santa Ana winds started to pick up in Ventura County. This year, though, it hit a little different. Premiums for their modest home in Simi Valley had jumped by nearly 35% since 2022. Suddenly, the idea of writing one big check for the whole year felt like a punch to the gut. Was it really better to pay annually, or should they switch to monthly payments?

Honestly, it’s a question Karl Susman at Los Angeles Insurance Quotes gets all the time. CA License #OB75129, phone (877) 411-5200. “People assume monthly is always more expensive,” Karl told me recently. “And often, it is. But the real answer is more complicated than just dollars and cents.”

Let’s talk about that sticker shock first. For most Californians, the biggest benefit of paying your insurance premium annually is the discount. Insurers — whether it’s for your car with AAA, your home with Farmers, or even a small business policy — often give you a break for paying in full upfront. Think of it like a bulk discount at Costco. You’re giving them the full amount of money right away, reducing their administrative burden of processing monthly payments, and removing the risk of you missing a payment mid-year. They pass some of those savings on to you. It’s not always a huge chunk, maybe 2% to 10% of your total premium, but on a $3,000 annual home insurance bill, that could be $60 to $300 back in your pocket. That’s real money.

The Annual Advantage: Saving a Little Something

The Chengs, for years, had dutifully paid their premiums annually. Mr. Cheng, a financial planner by trade, saw it as a simple math problem. If he could save $200 by paying it all at once, why wouldn’t he? He’d stash money away each month into a separate savings account, earmarking it for the insurance bill. When the bill came, the money was there. Done. No monthly reminders, no small processing fees tacked on, no worries about a payment bouncing.

This strategy works well for folks who are disciplined with their budgeting. You set aside a portion of your income specifically for that large, looming annual bill. Many people even align their insurance renewals with their tax refunds or a yearly bonus, making the lump sum payment less painful. It offers peace of mind, knowing that for the next 12 months, your coverage is locked in, paid up, and you don’t have to think about it again.

But here’s the thing. That lump sum can be substantial, especially these days. With property insurance premiums in places like the Inland Empire jumping due to wildfire risks, or auto rates creeping up across the Valley because of increased accident severity, that “discounted” annual payment can still feel enormous. A $4,000 annual home insurance premium, even with a 5% discount, still means writing a $3,800 check. For many families, especially those living paycheck to paycheck or facing other high costs of living in places like Los Angeles or San Diego, that kind of cash outlay simply isn’t feasible.

The Monthly Method: Spreading the Cost

That’s where monthly payments step in. Instead of one big hit, you get 12 smaller, more manageable charges. For the Chengs, looking at that $3,800 annual premium, breaking it into roughly $316 a month suddenly made it digestible. Their budget, already stretched thin by rising grocery prices and higher gas costs, could absorb $316 much easier than $3,800.

Most insurers offer monthly payment plans. Some do it directly, others work through a third-party financing company. This flexibility is a godsend for many. It helps smooth out cash flow and ensures you can maintain coverage without draining your savings or putting a strain on your credit cards. It means you don’t have to scramble to find a large sum of money once a year.

But wait — there’s a catch. Often, these monthly payment plans come with fees. Sometimes it’s a small administrative fee added to each payment, maybe $5 or $10. Other times, the discount you would have received for paying annually is simply removed, effectively making your total annual cost higher than if you’d paid in one go. It’s like paying interest, even if it’s not explicitly called that. Over 12 months, those small fees add up. That $60 to $300 you might save by paying annually? That’s the cost of convenience for going monthly.

California’s Unique Insurance Landscape

This decision becomes even more important in California’s wild and unpredictable insurance market. We’ve seen major insurers like State Farm and Farmers pull back from offering new home policies in certain areas, especially in high-risk zones near the foothills where wildfires are a constant threat. The FAIR Plan, our state’s “insurer of last resort,” has seen a huge surge in policies, and those premiums aren’t getting any cheaper.

Prop 103, while designed to protect consumers, also means that rate increases have to go through a rigorous approval process. But when they do get approved, they can be significant. Premiums jumped 40% between 2022 and 2024 for many homeowners. When you’re facing those kinds of increases, every dollar counts, and the choice between monthly and annual can feel like a really big deal.

Which brings up something most people miss. What if you need to cancel your policy mid-year? Say you sell your house in Orange County and move out of state. If you paid annually, you’ll usually get a prorated refund for the unused portion of your premium. If you’re paying monthly, you simply stop making payments. There’s no big refund coming, but then again, you never had that large sum tied up in the first place.

The Broker’s Perspective: Guidance Through the Maze

This is precisely where an experienced broker like Karl Susman becomes invaluable. Karl and his team at Los Angeles Insurance Quotes don’t just quote you a price; they talk through these kinds of payment considerations. They know the ins and outs of policies from various carriers — not just the big names, but also the smaller, more specialized insurers who might still be writing policies in tough areas like Paradise or parts of the Valley hit by recent fires.

“We always ask clients about their cash flow,” Karl explains. “It’s not just about finding the cheapest policy. It’s about finding a policy that fits their budget and their life. If paying monthly means they can keep their coverage without stress, even if it costs a little more overall, that’s a win.”

Sometimes, a client might be able to afford the annual payment, but they’d prefer to keep that lump sum in a high-yield savings account or an investment. The interest earned might offset the monthly fees. Other times, the financial pressure is real, and monthly payments are the only way to go. There’s no shame in either approach; it’s about what works for you.

Beyond the Price Tag: The Hidden Costs and Benefits

Think about the administrative burden. With annual payments, you get one bill, one payment, one confirmation. You’re done. With monthly, you have 12 transactions to track. Are you diligent about checking your bank statements? Do you have auto-pay set up? Missing even one payment can trigger late fees, or worse, a cancellation notice. While insurers are required to give you notice, it’s still a headache you don’t need.

For some businesses, especially smaller ones in places like downtown Sacramento or Long Beach, managing cash flow is paramount. A large annual insurance premium could tie up capital needed for payroll or inventory. Monthly payments, even with a slight premium, can be a smarter business decision, allowing funds to be deployed where they’re most needed.

But here’s a real scenario: Imagine the Chengs from Simi Valley again. They’re debating that annual payment. They could pay it all at once and save $200. Or they could pay monthly, keeping that $3,800 in their emergency fund. What if a sudden expense pops up – a major car repair, an unexpected medical bill? That $3,800 could be a lifeline. The $200 they might save on insurance suddenly feels less important than having readily available cash. It’s a trade-off, a financial balancing act.

Ultimately, the choice between monthly and annual payments isn’t just about saving a few dollars. It’s about personal finance, peace of mind, and fitting your insurance into your overall budget without undue stress. Before you make that decision, it makes sense to weigh the pros and cons for your specific situation.

If you’re wondering which payment plan makes the most sense for your California insurance, don’t guess. Talk to an expert. Karl Susman and his team at Los Angeles Insurance Quotes are ready to help you sort through your options. Get a personalized quote today: https://losangelesinsurancequotes.com/quote/

You don’t have to figure this out alone. For guidance on your California insurance needs, including payment options, reach out to Karl Susman, CA License #OB75129, at (877) 411-5200. Or start the process online: https://losangelesinsurancequotes.com/quote/

Frequently Asked Questions About Insurance Payments

- Do all insurance companies offer monthly payment options?

Most major insurance companies do offer monthly payment plans for auto, home, and other common policies. However, some smaller or specialty insurers, especially those in the high-risk property market, might only offer annual or bi-annual payment options. It’s always best to ask your agent or broker directly. - Will my credit score be affected by my payment choice?

Directly, no. Choosing monthly or annual payments doesn’t directly impact your credit score. However, consistently missing monthly payments can lead to policy cancellation, and if the insurer sends the unpaid balance to collections, that *will* negatively affect your credit. Paying annually avoids this risk entirely. - Can I switch from monthly to annual payments, or vice versa, mid-policy term?

Sometimes. Many insurers allow you to switch your payment plan during your policy term, though there might be administrative fees involved. If you switch from monthly to annual, you’ll need to pay the remaining balance in a lump sum. If you switch from annual to monthly, you’ll likely receive a prorated refund for the remaining annual payment, and then start making monthly installments (potentially with fees). - Are payment plans different for high-risk policies, like those through the FAIR Plan?

Yes, they can be. Policies through the California FAIR Plan, which often covers properties in high-wildfire-risk areas, can have stricter payment terms. While they do offer installment plans, the fees might be higher, or the initial down payment required might be larger compared to standard market policies. Always confirm the specific payment options and associated costs when dealing with such policies. - Is it true that my bank or lender can require me to pay annually?

For home insurance, yes. If you have a mortgage, your lender often requires proof of continuous insurance coverage and sometimes mandates that the premium be paid annually, especially if your insurance is escrowed. This ensures their investment (your home) is fully protected. They might even pay the annual premium directly from your escrow account.

This article is for informational purposes only and does not constitute financial advice.

Karl Susman, Los Angeles Insurance Quotes, CA License #OB75129